Our Blog

Understanding Parental Leave Pay and the New Superannuation Changes

Get Ready for Tax Time: Your WFH Questions Answered!

Tax time is just around the corner, and with it, important changes that could impact your financial future! Important Update: Division 296 – Superannuation Changes on the Horizon! As your trusted accountants, we're here to get you on the front foot, so let's dive into some superannuation news that's making waves. Proposed Division 296 Tax: What You Need to Know The Australian Government is proposing a new tax, called Division 296 (DIV296) , which is set to kick off on 1 July 2025 . This proposed tax looks to introduce an extra 15% tax on superannuation earnings that are attributed to super balances above a $3 million threshold. Key Takeaways: · Legislation Pending: This new tax has not yet been formally legislated, so it's a proposed change. · Proposed Start Date: 1 July 2025 (expected to be deferred) · Payment timing: If legislated, the first payments for Division 296 tax would not be due until after the end of the 2025–26 financial year. · Target: Individuals whose total super balances (TSB) exceed $3 million at the end of the financial year. · Tax Rate: An additional 15% on "earnings" above the threshold (on top of the current 15% fund tax rate). · "Earnings" Definition: Includes unrealised (paper) gains on your assets. It's not simply the profits you've actually made or locked in. Instead, it’s based on how much your super balance has increased over the year. · Non-Indexed Threshold: The $3 million limit won't increase with inflation. What Should You Do? While it is premature to make drastic changes before the legislation is passed, such as withdrawing money from super to avoid tax, give us a call or shoot us an email if you would like to better understand the implications of this potential change and how it may impact you.

Small Businesses Affected by Cyclone Alfred: You Could Be Eligible for $25,000 in Disaster Recovery Grants

💰 The ATO Might Owe You Money — Here’s How to Find Out Yes, you read that right. If you’ve paid your tax early , the ATO might actually owe you money in the form of Interest on Early Payments . This isn’t a scam, a loophole, or something shady. It’s legit, and it’s laid out on the ATO’s website for all to see. But most people never know to look for it. Here’s the deal: What is “Interest on Early Payments”? If you pay tax before the due date (think PAYG instalments, GST, income tax, etc.), the ATO will calculate interest on the early payment from the date you paid to the due date. So yes, paying early could earn you a small return 💸 You’re eligible if: You paid a tax bill before its due date You lodged a tax return that resulted in a debit , not a refund, and paid early How is it paid? If you're eligible, you won't receive a cheque in the mail (sorry). The interest is: Credited to your ATO account , or Can be requested , depending on how you lodged If you lodge through us, good news, we’ll keep an eye on that. But if you’ve done something early yourself, or just want to check, here's how to DIY like a boss: How to check your ATO balance & early payment credits: 🔗 Check your account balance on the ATO website 🔗 How to request a refund or credit transfer Need to make a payment? 🔗 Get your payment reference or payment slip TL; DR (Too Lazy; Didn't Read): Pay early = possible ATO interest Not automatic, but you can check it Links above will show you everything Still confused? Check the article again... it’s all there 😉

Some of the key changes for Super Funds in the 2024-2025 financial year are:

6 important dates for employers for the end of this financial year.

The ATO announces its priorities for Tax Time 2024.

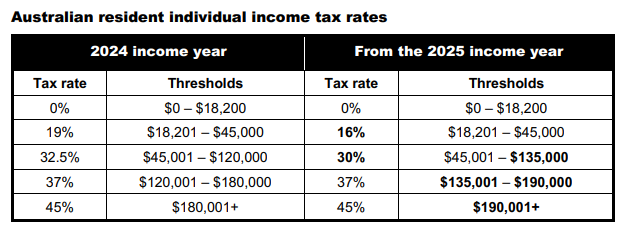

1. Personal income tax measures

Carry-forward contributions provide flexibility for effective retirement planning, especially for those with unconventional work histories. By utilizing unused caps, you can optimize your contributions while minimizing tax implications.